This is how the real estate market in the Ruhr region is developing

The challenges in the German property market also affected property transactions in the Ruhr area in 2023. The property market recorded fewer new buildings and transactions last year, but the Ruhr area proved more resilient than other top locations in Germany.

The volume of commercial property transactions in the Ruhr Metropolis in 2023 is just under €1.3 billion, around 28% below the previous year's level. Compared to the A-cities, the decline in the Ruhr area was much more moderate. In the ranking of Germany's top property locations, the Ruhr area has thus moved up to second place behind Berlin.

Wide range in rents

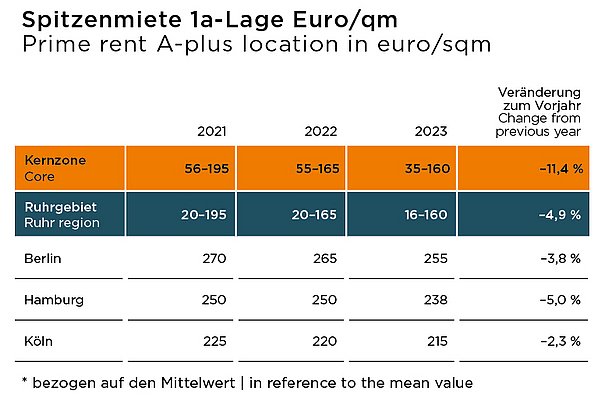

Rents for office properties showed a wider range: Top rents in the core cities of the Ruhr area continued to rise, ranging from EUR 16.50 to EUR 21.00/sq m - an increase of 7.9%. Even higher rents could be achieved in the foreseeable future for newly built space in prime locations.

Logistics market provides dynamic

In 2023, almost 565,000 m² of logistics space was completed in the Ruhr Metropolis. The Ruhr area thus defied the difficult conditions for project development and recorded the highest volume of new construction since 2017, when around 750,000 m² was realised.

Key figures for each real estate class

Asset classes: Overview & Development 2023

Office property market

The weak economic phase had a significant negative impact on take-up in all seven A-cities. In the Ruhr Metropolis, the decline of around 21 per cent to a total of 443 thousand m² was still moderate compared to the A-cities.

New office properties

New office space in the Ruhr metropolis has decreased by approximately 30% compared to 2022. In 2022, the highest figure since 2010 was recorded with around 278,000 m² of MF-GIF, while in 2023, the figure was only around 192,000 m². The construction of new office space has almost come to a standstill in some cases, such as in Essen (6,650 m²). Plans without relevant pre-letting are being scrutinised, particularly in the seven A cities. The influx of new office space in the foreseeable future may be dampened by a number of insolvencies. Property and project developers are still in a crisis situation. The wave of insolvencies in Germany is expected to peak in 2024. Several companies with projects in the pipeline and a medium-term realization horizon are affected in the office segment. Overall, the impact on the Ruhr metropolis is expected to be less significant than in some major cities. However, it can be assumed that the pipeline in the Ruhr metropolis will also decrease in the short to medium term due to the weaker economy and more challenging framework conditions for project development.

Vacancy rate

The increase in job openings that started during the COVID-19 pandemic persisted in 2023, albeit at a slower rate. The overall vacancy rate for the Ruhr Metropolis was 5.1%, which is only 0.2 percentage points higher than the previous year. Bochum had the largest increase among the core cities, from 3.2% to 4.4%, with a total of 32,000 square meters. While Dortmund and Essen saw slight increases in vacancies (Dortmund +4,000 m² to 5.1% and Essen +5,000 m² to 7.3%), vacancies in Duisburg decreased (-12,000 m² to 3.3%). The increase in space available for short-term occupancy was due to vacancies and space consolidations. Sublet space also remains important.<o:p></o:p>

Office space take-up in the Ruhr Metropolis amounted to approximately 443,000 m² in 2023, which was below the 10-year average of 510,000 m². After Berlin, the Ruhr Metropolis recorded the highest take-up of office space. The lower take-up is due to the weak economic phase and associated uncertainties, resulting in fewer large-volume deals and owner-occupier construction starts. Compared to most A-cities, the decline in the Ruhr area was comparatively moderate.<o:p></o:p>

Only Essen achieved take-up of over 100,000 m², out of the driving forces of the past. Dortmund did not keep up with the brisk market activity of 2021 and 2022, with a take-up of only 85,000 m². Bochum and Duisburg, on the other hand, exceeded their respective 10-year averages, with 73,500 m² and 71,000 m², respectively.

Contracts in the office market

The four main office markets accounted for 339,500 m², which is approximately 77% of the total take-up. Essen, in particular, contributed significantly to the total take-up with 110,000 m². This was mainly due to several major deals and large-volume owner-occupier lettings in the first half of the year. The City of Essen has leased approximately 17,400 m² of office space in 'The Brix' property. E.ON has leased approximately 9,000 m² of office space, while Siemens and RWE have each leased 5,600 m². Additionally, construction has begun on the FOM University administrative building in Essen, which will be approximately 6,600 m² in size.

The decrease in office space uptake in Dortmund, which was around a third less than the previous year, can be attributed to the absence of significant deals and owner-occupier construction starts. These factors had previously resulted in significantly above-average outcomes. In 2023, three deals for more than 5,000 m² were registered. The most significant of these was BIG's direct letting of 7,400 m² in the Südtor project on Lake Phoenix. Subsequently, the City of Dortmund leased 6,900 m² in the RWE Tower, followed by the Dortmund tax office leasing 5,300 m².

In 2023, Duisburg surpassed its 10-year average of 64,000 m² by recording 71,000 m² of office space take-up. The public sector accounted for most of the major deals concluded. The most significant deal last year was the letting of over 10,000 m² to the Public Order and Social Welfare Office in Friedrich-Willhelm-Strasse. Furthermore, the Bau- und Liegenschaftsbetrieb NRW rented approximately 7,750 m² in the Silberpalais, and the Verwaltungs-Berufsgenossenschaft commenced construction of the Torhaus Süd, which will cover around 5,000 m².<o:p></o:p>

Although Bochum did not match the record year of 2022, it still achieved an above-average letting performance of 71,000 m², consisting of agreements in the smaller to medium-sized space segment.

Rents

Although vacancy rates are increasing, achievable prime rents continue to show a positive trend. In core cities, they range from EUR 16.50 to EUR 21.00/m². The slight growth in prime rents will continue in the smaller submarkets of the Ruhr Metropolis until 2023. It is foreseeable that even higher rents could be achieved for new-build space in prime locations. Users are increasingly demanding better location and quality of properties and are willing to pay higher prices for them. This trend is supported by the persistently high construction costs, which are reflected in correspondingly higher rents. This mirrors the trend in the seven A-cities, where rental prices and vacancy trends have also decoupled.

Investment Market

As anticipated, the subdued transaction activity from the first half of the year persisted in the investment market. The investment volume in the office segment was approximately 54% lower than the previous year, at around €421 million. The Ruhr area experienced a smaller decline compared to the A-cities. Following last year's peak in interest rates, the investment market is expected to recover in 2024. The stabilisation of interest rates will provide investors with the necessary planning and calculation security.

Prime yields for office properties in the Ruhr Metropolis rose more moderately in 2023, up to 70 basis points, compared to the A-cities, which recorded premiums of 80 to 100 basis points. The pricing process is expected to enter its final phase in 2024, and the price corrections should be completed. Overall, only marginal increases are expected.

Retail

In the Ruhr Metropolis and many German shopping centres, there are not only shop closures but also reductions in floor space. The number of retail storeys is decreasing because concepts are being revised or space productivity has fallen, making it impossible to generate the sales required to meet the rents demanded. The focus is increasingly on ground floor areas, as these have the highest customer frequency. There are increased risks in terms of re-letting or the need to reallocate lower and upper floors to other uses, which reduces the earnings prospects.

Retail Frequency

The impact of the coronavirus pandemic on city centre retail seems to have been forgotten. Retail footfall has returned to a stable, high level and is even higher than in 2019 in many places. The focus has shifted towards new retail concepts occupying prime city centre locations in A- and B-cities, as well as shopping centres. Additionally, gastronomy and discount retail concepts are becoming increasingly interested in prime city centre locations. The recent insolvency of Galeria has brought attention to the decline of formerly dominant city centre retail businesses. While some will remain open, the future of these once glamorous large-scale stores is uncertain. This will likely result in a reorganization of customer flows in many city centres and a realignment of department store neighborhoods. The near future will bring significant changes to many city centres, which will have far-reaching effects on the sector and tenant structure of these areas.

The expectation that internet-based retailers would enhance city centre locations with their own physical stores has not been met. In fact, some retailers have separated from their brick-and-mortar stores or have had to withdraw from them due to consolidation, and are now focusing solely on their online presence. However, certain category leaders such as TJ Maxx and Zalando Outlet are still expanding their physical store concepts. In smaller cities and towns, price-focused retailers are increasingly establishing themselves in city centre pedestrian zones, which is affecting achievable rent levels.

Rents

The increase in job openings that started during the COVID-19 pandemic persisted in 2023, albeit at a slower rate. The overall vacancy rate for the Ruhr Metropolis area was 5.1%, which is only 0.2 percentage points higher than the previous year. Bochum had the highest increase among the core cities, from 3.2% to 4.4%, with a total area of over 32,000 m². Dortmund and Essen experienced slight increases in vacancies, with Dortmund increasing by 4,000 m² to 5.1 % and Essen increasing by 5,000 m² to 7.3 %. On the other hand, Duisburg saw a decrease in vacancies, with a reduction of 12,000 m² to 3.3 %. The increase in available space for short-term occupancy was due to vacancies and space consolidations, with sublet space also remaining important.

Office take-up in the Ruhr Metropolis amounted to approximately 443,000 m² in 2023, which is below the 10-year average of 510,000 m². Despite this, the Ruhr Metropolis area still recorded the second-highest take-up of office space after Berlin. The lower take-up can be attributed to the weak economic phase and associated uncertainties, resulting in fewer large-volume deals and owner-occupier construction starts. Compared to most A-cities, the decline in the Ruhr area was relatively moderate.

Of the driving forces of the past, only Essen achieved a take-up of over 100,000 m². Dortmund's take-up of 85,000 m² did not match the brisk market activity of 2021 and 2022. Bochum and Duisburg exceeded their respective 10-year averages with 73,500 m² and 71,000 m², respectively.

Market for logistics properties

Overall, the logistics market in the Ruhr Metropolis continues to be very dynamic. Demand for space is robust and is above the long-term average despite the lack of economic stimulus. Rents continue to show a clear upward trend, which is likely to continue until 2024 in view of the excess demand.

Completions

In 2023, almost 565,000 m² of logistics space was completed in the Ruhr Metropolis. The Ruhr area thus defied the difficult conditions for project development and recorded the highest volume of new construction since 2017, when around 750,000 m² was completed. The district of Wesel (155,500 m²) leads the completion statistics, followed by the districts of Recklinghausen (102,800 m²) and Unna (97,100 m²). Dortmund (80,200 m²), Duisburg (60,300 m²) and Oberhausen (50,000 m²) also recorded significant volumes of new take-up.

Space Turnover

Demand for space was also unaffected by the economic downturn and amounted to around 510,000 m² last year. Although this is a good 9% less than in the previous year, the ten-year average was exceeded by a good 13%.

Market-defining deals were concluded last year in Bottrop (57,000 m² by Yusen Logistics), Schwelm (45,000 m² by a production company), Dortmund (30,000 m² by pfennig logistics) and Bönen (27,000 m² by Recht Kontraktlogistik).

Rents

Excess demand continues to drive up rents in all submarkets of the Ruhr Metropolis. At the top end, rents of up to EUR 7.60/m² can be achieved for large warehouse space in the core logistics area of the Ruhr Metropolis. Occasionally rents of over 8.00 euros/m² have been achieved for built-to-suit logistics solutions. There are still hardly any vacancies in modern logistics properties in the Ruhr area, although marketing times have lengthened slightly over the course of the year. No significant easing of the supply situation is expected in the short term, which suggests that rents will continue to rise.

The logistics segment was unable to escape the shock paralysis on the commercial investment markets. The total transaction volume for logistics, industrial and corporate properties in the Ruhr Metropolis area fell sharply to around EUR 322 million in 2023, a decline of around 40% compared with the previous year.

The decline was already visible in 2022. However, the uncertainty caused by the interest rate shock did not have a real impact on the investment market until 2023. Nevertheless, a cautious recovery was observed in the second half of the year, after only €128 million of logistics and industrial property was transacted in the first half of 2023.

The price corrections that began in 2022 continued last year. Net initial yields rose by 40 to 70 basis points, depending on the submarket. Duisburg remains the most expensive location at 4.70%, followed by Dortmund at 5.00% and Essen at 5.20%.

Overall, the logistics market in the Metropolis Ruhr remains very dynamic. Demand for space is robust and has exceeded the long-term average despite the lack of economic stimulus. Rents continue to show a clear upward trend, which is likely to continue until 2024 given the excess demand.

The outlook for the transaction market is therefore also positive. After interest rates peaked last year, the financing environment should stabilise this year and investor confidence should return.

When analysing market data in the logistics and corporate real estate segments, the respective logistics regions are used as a spatial aggregate and therefore not only the respective core cities are considered. This means that transactions or projects in the surrounding areas of the respective market cities can also be included. For example, the Ruhr area is made up of the Rhine-Ruhr and Dortmund logistics regions.

Corporate real estate

The trend of declining completions for corporate real estate continued in 2023. Due to the difficult conditions for project developments, the volume of new construction fell by around 45% to just under 59,000 m² of net lettable area. Take-up in the Ruhr area halved compared with the previous year, mainly due to the shortage of space and the weak economy. Nevertheless, rents are rising slightly, especially for office, social and flex space in modern business parks that score points for their high sustainability standards. Third-party usability, reversibility and ESG standards are now fundamental requirements for contemporary properties, while older existing properties are becoming less marketable.

Definition

Business properties are mixed-use commercial properties with a typical medium-sized tenant structure. The mix includes office, storage, manufacturing, research, service and/or wholesale space, as well as open space.

The heterogeneity and variety of uses make this asset class difficult to track.

The business property segment includes distribution properties (< 10,000 m²), production warehouses (< 10,000 m²), business parks and transformation properties.

Completions

The trend of declining corporate property completions in the first half of the year continued during the rest of the year. As a result of project postponements due to the difficult economic environment, the volume of completions at the end of the year amounted to 58,850 sqm of net lettable area. The environment for development projects in the corporate real estate segment remains challenging. In addition to the limited availability of space, high construction costs and changed financing conditions, there is currently no economic tailwind to stimulate demand. Purely speculative project developments are the exception in the current market environment.

In 2023, take-up of corporate property in the Ruhr area will have more than halved compared with the previous year. In addition to the lack of available space, the main reason for the sharp drop in take-up is the economic downturn.

Despite the difficult market environment, rents continue to rise slightly. The highest rents are being achieved for office, social and flex space. Flex space with high sustainability standards, such as those found in modern business parks, continues to be a promising market as it can potentially appeal to a wide range of user groups, thereby diversifying risk. Third-party usability, reversibility of use and compliance with ESG standards are more than ever seen as fundamental requirements for contemporary properties. As a result, the marketability of older existing properties in particular is limited. Modern properties should benefit from further rent increases in the future.

Price corrections in the corporate property segment will continue in 2023. Net initial yields have risen by 40 to 90 basis points, depending on location and property type. With interest rates having peaked for the time being last year, price corrections in 2024 are likely to be much more moderate. The yield gap between modern, sustainable properties and those with significant ESG deficits is likely to widen further.

Investment market in the Ruhr Metropolis

The uncertainties caused by the interest rate shock had a significant impact on the transaction markets. As a result, less capital was invested in commercial property compared to the previous year. Investment turnover in the Ruhr Metropolis was €1.3 billion, which is approximately 28% lower than the previous year. In contrast, the volume in the seven A-cities decreased by around 67% to €8.4 billion. The office segment ranked first in terms of turnover, with around 421 million euros or 32.4% of the total. Retail properties came in second with 397.6 million euros or 30.6%, followed by logistics/production with 322 million euros or 24.8%.

Transaction volume

In 2023, commercial property transactions in the Ruhr Metropolis area amounted to just under €1.3 billion, a decrease of 28% compared to the previous year. However, the decline in the Ruhr area was much less severe than in the A cities. As a result, the Ruhr area has moved up to second place in the ranking, behind Berlin, which once again leads the way with around €3.1 billion.

Nationwide, there has been a significant slowdown in transaction activity, resulting in the weakest investment turnover in Germany since the years shortly after the financial crisis. In 2023, approximately €23 billion was transacted in commercial property, compared to €51.8 billion in 2022.

The decline in transaction activity was not unexpected, given the changes in the capital market environment. This trend had already become apparent in the second half of 2022. The uncertainty surrounding further interest rate hikes and the ongoing pricing phase had a significant negative impact on transactions. In many cases, buyers and sellers were unable to agree on a purchase price that was adapted to the new market environment, and transactions were not finalised.

The office segment was the top-performing asset class, accounting for approximately €421.1 million or 32.4% of sales. Retail properties followed closely behind with €397.6 million or 30.6%.

Selected transactions

The trend of declining corporate property completions in the first half of the year continued during the rest of the year. As a result of project postponements due to the difficult economic environment, the volume of completions at the end of the year amounted to 58,850 sqm of net lettable area. The environment for development projects in the corporate real estate segment remains challenging. In addition to the limited availability of space, high construction costs and changed financing conditions, there is currently no economic tailwind to stimulate demand. Purely speculative project developments are the exception in the current market environment.

In 2023, take-up of corporate property in the Ruhr area will have more than halved compared with the previous year. In addition to the lack of available space, the main reason for the sharp drop in take-up is the economic downturn.

Despite the difficult market environment, rents continue to rise slightly. The highest rents are being achieved for office, community and flex space. Flex space with high sustainability standards, such as those found in modern business parks, remains a promising market as it can potentially appeal to a wide range of user groups, thereby diversifying risk. Third-party usability, reversibility of use and compliance with ESG standards are more than ever seen as fundamental requirements for contemporary properties. As a result, the marketability of older assets in particular is limited. Modern properties should benefit from further rental growth in the future.

Price corrections in the corporate property segment will continue in 2023. Net initial yields have risen by 40 to 90 basis points, depending on location and property type. With interest rates having peaked for the time being last year, price corrections in 2024 are likely to be much more moderate. The yield gap between modern, sustainable properties and those with significant ESG deficits is likely to widen further.

Note: The calculation of the prime rent is based on the definition of the Gesellschaft für Immobilienwirtschaftliche Forschung e.V. (Society for Real Estate Research). In the markets, deals are also achieved above the prime rent median.

Who participates in the real estate market report?

In addition to the economic development agencies of the municipalities from the Ruhr Metropolis, established brokerage companies are also participating:

Contact for the real estate market in the Ruhr area

Our Sites & Investors Service team will be happy to help you with any questions you may have about the real estate market in the Ruhr area and to advise you on the following topics:

- Market information

- Location data

- Analyses of sites

- Location searches

- Matching investors & companies

This could also be interesting:

Location Search and Investor Service

Request NowYour contact for the Real Estate Market Report Ruhr

Corporate Communications, Press Spokesman